Click the Green Editorial Tab Above!

Interest Rates Are Moving Up, How Does That Impact You? by PPCLOAN's Steven Kemper..

2011 Q1

First Quarter 2011

As noted in the Fourth Quarter 2010 Allstate Agency Value Index Report, the stock market finished 2010 on a strong note in spite of the significant depressed jobs and housing headwinds. The First Quarter 2011 seems to have produced much the same result as the Dow and S&P Indexes both increased over 5% despite continued problems with jobs and housing, and the addition of Mideast turmoil and the devastating Japanese earthquake.

Interest rates have also remained stable from Quarter to Quarter, and it is expected that the accommodative monetary policy will continue over the near term as FRB Chicago President Charles Evans noted in March 2011, “When we look at the past two years as a whole, the improvements have been disappointing,…Too many people remain unemployed – and some for extended periods – and too many businesses have not yet returned to full operations.”

Reflecting this relatively stable climate is the value for which Allstate agencies were sold relative to their renewal commission revenues, continuing the recent trend of stabilization. The simple average agency value multiple for the first quarter of 2011 was 2.47 compared to 2.41 and 2.43 for the fourth and third quarters of 2010, respectively. During the first quarter, PPC LOAN processed far fewer small agency acquisition financing transactions relative to the number of large agency transactions. Consequently, the degree to which this seemingly anomalous acquisition transaction mix effected the simple or weighted average that the agency value multiple moved relative to the prior quarter’s results, is less important than the fact that, as noted, the trend of stabilizing values has continued.

| Allstate Agency Price to 12MM Earned Premium Ratio (National Average) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| Use the arrows to see agency values over time. | prev next |

Agency Analysis by Size Group

$0 to $100,000 in New/Renewal Commission

Coming off of a sharp drop in value in the fourth quarter, smaller agencies continued to take a beating, having their average value drop to 1.78 – an all-time low since we began tracking values in 2006. However, it is important to note that this size group had the lowest number of agency transitions involving PPC LOAN during the first quarter of 2011, leaving the possibility for this drop to be a statistical anomaly.

$100,000 to $200,000 in New/Renewal Commission

Agencies in this group continue to see an increase in value, which can be directly attributed to the growing number of allowed merger transactions. Historically, the majority of agencies transitioned as part of a merger transaction was limited to the smallest agencies. Recently, however, agencies in this size group have been part of merger transactions for outside buyers and existing agents. This phenomena drives home the theory that any agency being transitioned as part of a merger transaction will likely result in an increased value relative to the agency being sold as a stand-alone agency.

$200,000 to $300,000 in New/Renewal Commission

Agencies in this size group seem to be the most stable, as the average value continues to gravitate towards a 2.50 multiple of renewal commission income.

The evidence of the buyers’ preference for larger Allstate agencies is on clear display, as they offer new owners ample cash flow to cover routine operating costs, their own living wage needs and agency acquisition debt servicing costs with plenty to spare for investments in organic growth initiatives.

$300,000+ in New/Renewal Commission

Agency values in this size group continued to hold strong at approximately 2.75 times renewal commission income. Buyers have a preference for larger sized agencies, however, the days of buying on impulse seem to be gone. Today, buyers are focused on an agency’s historical cash flow (“Economic Value”) and give little or no weight to the future potential of the agency when looking to make a purchase offer.

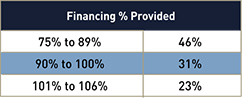

Further stated, the market value of Allstate agencies, for which willing buyers and sellers are reaching an agreement on price, is very near the agency economic value, i.e., what the cash flow will support,, implying that the transitions occurring today are economically sound and much less likely to result in Agency transition failures due to insufficient cash flow.

| Allstate Agency Value Ratios | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| Use the arrows to see agency values over time. | prev next |